Why Financial Literacy in India is important?

23rd April 2024 | Author : Centricity

“Financial literacy gives you the opportunity to be confident & empowered to live the quality of life you’ve worked for!”- Erin Beable

Imagine the economic growth of a developing country, where everyone would have access to financial information and be capable of making wise financial decisions. This would lead to a more stable and prosperous economy.

As per reports, it is stated that India only consists of 27% of the population that falls into the category of “financially literate”. According to this, one out of every five Indians is capable of addressing one of the most critical aspects of human well-being.

Often, it is believed that financial literacy only lacking within the marginalised or economically impoverished sections of the society. However, it is not completely true. This is a challenge that upper & majorly middle-class people face!

The lack of financial literacy, however, contributes to social inequality for the economically backward. For individuals to access and effectively use financial services, it may be necessary to have a basic understanding of financial concepts.

With financial literacy, citizens can make informed financial decisions that benefit themselves and their communities. It can also help to reduce poverty and inequality, as people can make informed decisions about investments, savings, and borrowing. This, in turn, can lead to a more sustainable and prosperous economy.

Scope and Importance of Financial Literacy

India is a nation in development. Even in the post-Covid-19 Era, we have had notable economic progress. It stands for India's capacity for national development and its likely future domination of the world stage.

Despite India’s wonderful accomplishments, certain businesses in the nation—mostly those in small and medium-sized industries—continue to struggle to thrive in this fiercely competitive market. For Indian business enterprises, financial mismanagement and inadequate financial planning have always been problems.

There is still room for improvement when compared to other developing and developed nations worldwide. It is necessary to determine the causes of this low penetration of financial literacy. The main causes of India's low financial literacy rate might be attributed to interstate differences as well as a lack of formal education and awareness.

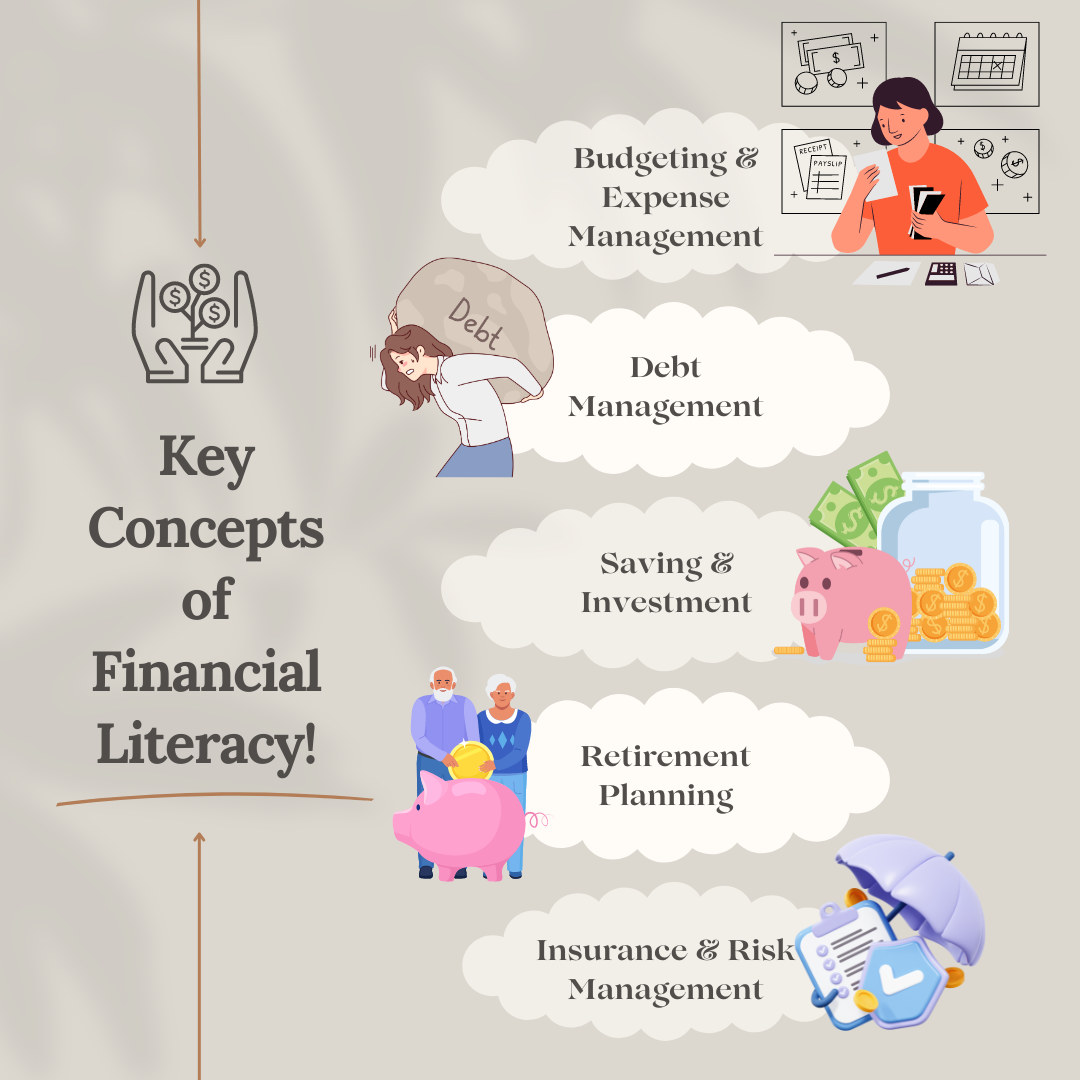

Financial literacy is the ability to comprehend and make effective use of financial concepts and skills in day-to-day living. Financial management, credit management, investing, and budgeting are all fundamental skills that everyone should possess.

How will Financial Literacy help in India?

What should be done about financial literacy?

- Improving financial literacy in India requires a multifaceted approach involving both governmental and non-governmental efforts. By adopting a comprehensive approach that combines education, technology, collaboration, and community engagement, India can make significant strides in improving financial literacy across the country.

- Introducing financial literacy as a part of the school curriculum can ingrain basic financial concepts from an early age. This can include topics like budgeting, saving, investing, and understanding credit.

- Organize workshops, seminars, and awareness campaigns at various levels targeting different demographics, including rural and urban populations. These programs should be designed to cater to the specific needs and understanding levels of different groups.

- Utilize digital platforms and mobile apps to disseminate financial education. Interactive mobile apps and online courses can make learning about financial concepts more engaging and accessible, especially for the younger generation.

- Enhance efforts to promote financial inclusion, ensuring that all segments of society have access to basic financial services. This includes initiatives to increase banking penetration, promote microfinance, and expand access to insurance and pension schemes.

- Educate consumers about their rights and responsibilities when it comes to financial products and services. This can help prevent exploitation and empower individuals to make informed financial decisions.

In conclusion, financial literacy is not just important for individual prosperity but also the overall economic development of India. By equipping citizens with the knowledge and skills to make sound financial decisions, India can unlock its full economic potential and improve the financial well-being of its people.

Thematic Funds in India: A Growing Trend in Investment!

30th January 2025

Are you investing in SIPs smartly ?

21st January 2025

Multi-Asset Funds in India: Diversification Made Easy for Investors

16th December 2024

Multi-Cap vs Flexi-Cap Mutual Funds: Where to Invest in 2024?

26th September 2024